I am building an R package that has Boost and QuantLib dependency. It is a library package, which took me a while to compile in R. I thought it might be interesting to share my experience with others. I came up with the following solution that works for a Windows 64-bit platform. Here are the instructions:

- Download and install R from: http://cran.r-project.org/bin/windows/base/

- Download and install latest version of Rtools from: http://cran.r-project.org/bin/windows/Rtools/

- Download and install MikTex from: http://miktex.org/download

- Add to System Environment PATH: to R, example: C:\R-3.1.2\bin; to RTools, example: C:\Rtools\bin;c:\Rtools\gcc-4.6.3\bin;C:\Rtools\gcc-4.6.3\i686-w64-mingw32\bin; to perl, example: to miktex, example: C:\Program Files (x86)\MiKTeX 2.9\miktex\bin; Control Panel -> System -> Advanced System Settings -> Advanced -> Environment Variables Edit path variable by appending paths after ;

- Download Boost and build it with Rtools

- Unpack loaded code

- Open command line Win+R -> cmd.exe

- Change current folder to your Boost folder. For example, cd C:\libraries\boost_1_57_0 4. Type command: bootstrap mingw

- Type command: b2 toolset=gcc address-model=3. Your compiled libraries are now in stage/lib subfolder

- Type command: b2 toolset=gcc address-model=64. Your compiled libraries are now in stage/lib subfolder

- In case you have problems due to missing ml, make sure MASM and MASM64 (ml.exe and ml64.exe) are available in PATH. This should be in the C:\Program Files (x86)\Microsoft Visual Studio path

- Download QuantLib and build it with your version of Boost headers. You can download QuantLib from http://quantlib.org/ make sure to download the .tar.gz file. Here we have loaded QuantLib-1.5

- open msys and run the following instructions

- cd C:/Working/QuantLib

- tar xzvf QuantLib-1.4.tar.gz. Also make sure that the path to mingw is set to the one in Rtools

- open msys, run the following instructions:

- cd C:/Working/QuantLib/QuantLib-1.4

- configure CXX=’g++ -m32′ CXXFLAGS=’-g -O2 -std=c++0x’ –with-boost-include=C:/Working/boost/boost_1_57_0 –prefix=C:/Working/QuantLib/QuantLib-1.4

- Build the same library for x64 architecture: CXX=’g++ -m64′ CXXFLAGS=’-g -O2 -std=c++0x’ Note that you should have around 5GB of free space for successful compilation

- open msys and run the following instructions

- Create a folder for your package

- Create three folders: R, man, src

- Create or update DESCRIPTION file with information about the package, its author, and link libraries

- Copy the code you need to build the function into the src folder

- If the original code could be compiled without issues with Rtools compiler (mingw), you should only add dllmain.cpp with defined dllentry

- Make a file named NAMESPACE in the root directory. There we define which dlls we need for the package to work (useDynLib) and what we should export from them (export or export pattern). Also we should identify which R packets we should import (import)

- R package run:

- Write wrapper on R to call function from dll

- To make documentation, open R. Type install.packages(‘roxygen2’). Change folder to your package root folder. Type roxygen2::roxygenise().

- Create file Makevars.win to build your package library in the windows environment. In this file it is very important to set following the variables: SOURCES, OBJECTS, PKG_CPPFLAGS, PKG_LIBS. These variables will be updated as you continue to develop your code. Of course, you can add additional build targets. SOURCES is an enumeration of all cpp files you need to build your function from the project (including dependencies). You should update this variable whenever you add additional cpp files. OBJECTS is an enumeration of object files compiled from SOURCES. PKG_CPPFLAGS is the set of flags used for code compilation, including paths to include files. Note we also use the -std=c++0x flag for Boost compatibility. Here the $(shell RScript -e Rcpp:::CxxFlags()) command helps access R and Rcpp include files. You should update this variable whenever you add new h or hpp files to build. PKG_LIBS is the set of flags used for code linking, including paths to additional libraries. $(shell RScript -e Rcpp:::LdFlags()) helps to link Rcpp libraries. You should update this variable whenever you require the use of a new library in your code

- Prepare environment. For some reason in current version of R, makefile for package uses only gcc for linking. And we need to use g++ to support template functionality of boost %.dll: replace line 216 in \etc\i386\Makeconf and in \etc\x64\Makeconf $(SHLIB_LD) -shared $(DLLFLAGS) -o $@ $*.def $^ $(ALL_LIBS) with $(SHLIB_CXXLD) -shared -o $@ $*.def $^ $(ALL_LIBS) or replace line: CC = $(BINPREF)gcc $(M_ARCH) with CC = $(BINPREF)g++ $(M_ARCH)

- If you successfully complete all the previous steps, you can verify your package. Open command line Win+R cmd.exe. Change current folder to your package parent folder. Type: R CMD check

is the local variance,

is the local variance,  is the strike, and

is the strike, and  is the maturity.

is the maturity.  is the log moneyness strike where

is the log moneyness strike where  is the forward and

is the forward and  is the implied total variance. As seen in the above equation, the local volatility is a function of the implied volatility rather than call/put prices. This approach is much more useful in practice.

is the implied total variance. As seen in the above equation, the local volatility is a function of the implied volatility rather than call/put prices. This approach is much more useful in practice. , we have:

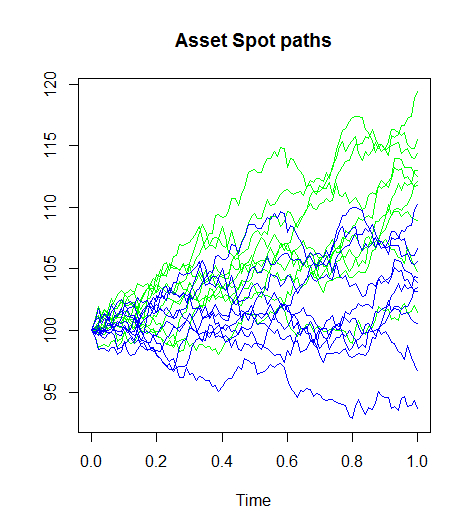

, we have:![E[S_t | \Im_0]=S_0](https://s0.wp.com/latex.php?latex=E%5BS_t+%7C+%5CIm_0%5D%3DS_0&bg=ffffff&fg=444444&s=1&c=20201002)

is the filtration (or the set of scenarios that could happen up to time 0) and

is the filtration (or the set of scenarios that could happen up to time 0) and  is the asset price at time t. In a risk neutral world the expected future value of an asset is its value today. This result is a consequence of the no-arbitrage principle. If the expected future price of the asset is different from its current price, the market would purchase or sell the asset until it reaches the equilibrium level. Hence the risk neutral probability is based on the reachability of an asset.

is the asset price at time t. In a risk neutral world the expected future value of an asset is its value today. This result is a consequence of the no-arbitrage principle. If the expected future price of the asset is different from its current price, the market would purchase or sell the asset until it reaches the equilibrium level. Hence the risk neutral probability is based on the reachability of an asset. and volatility

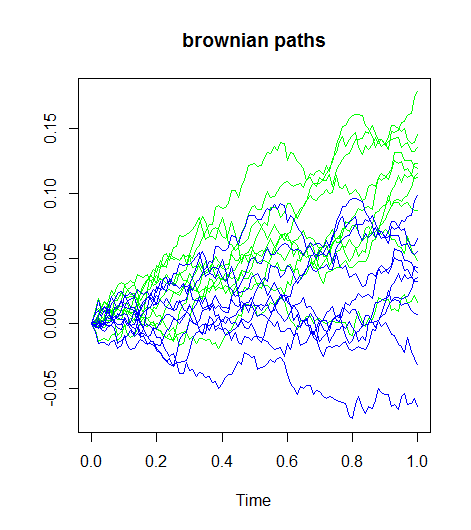

and volatility  . The relationship between a Brownian path in the historical world

. The relationship between a Brownian path in the historical world  and the risk neutral world

and the risk neutral world  is a shift in the drift:

is a shift in the drift: